Suppose that an insurer has an exponential utility function $u(x)=−2e^{-2x}$. What is the minimum premium $P^{-}$ to be asked for a risk X?

After solving this we reached the following,

So,only need help to solve the last step.

Suppose that an insurer has an exponential utility function $u(x)=−2e^{-2x}$. What is the minimum premium $P^{-}$ to be asked for a risk X?

After solving this we reached the following,

So,only need help to solve the last step.

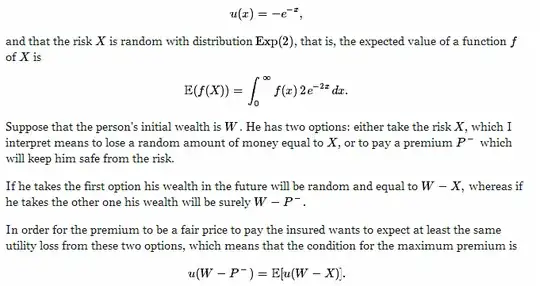

The utility function is $u(x) = -e^{-x}$ which is concave. The person is risk averse and will pay the premium to avoid loss. The loss has an exponential distribution with expectation

$$E[X] = \int_{0}^{\infty}2xe^{-2x}dx = \frac{1}{2}.$$ The premium is determined by

$$u(W-P^-)=E[u(W-X)] .$$ Substituting the utility function

$$-e^{-(W-P^-)}= \int_{0}^{\infty}[-e^{-(W-x)}]2e^{-2x}dx = -e^{-W}\int_{0}^{\infty}2e^{-x}dx=-2e^{-W}$$

Hence,

$$e^{P^-}=2\\\ P^- = \ln(2) $$

So the premium is $\ln(2)$ which is slightly larger than the expected loss.