I don't really like using conditional probability. I prefer indicator variables or partitions. I totally get your confusion and hope that I have understood your confusion as well.

Firstly, let's partition $\Omega$ by using $T$, i.e. let's identify the kinds of events in terms $T$: For any $\omega \in \Omega$, we must have $\omega$ be in exactly one of the following cases:

$$1.) \ 0 \le T<1.5$$ $$2.) \ 1.5 \le T<8$$ $$3.) \ 8 \le T<10$$

Why do we do this instead of something like $T\in[0,1], T\in[1,2], ..., T\in[9,10]$? This is because the way the range of $W$ is partitioned. It may be helpful to write $W$ as follows:

$$W = 0 \times 1_{0 \le T<1.5} + 100e^{-0.04T} \times 1_{1.5 \leq T < 8} + 0 \times 1_{8 \le T<10}$$

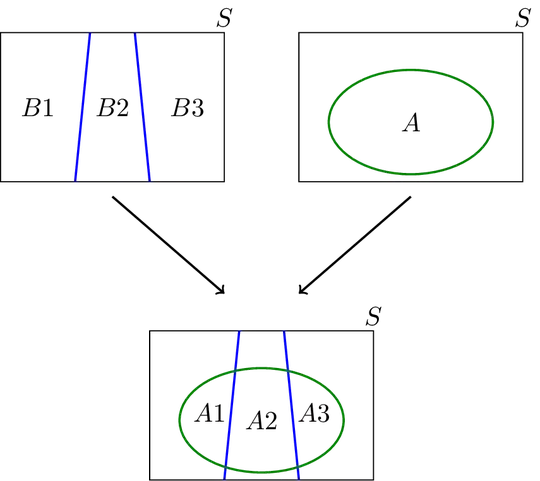

Going back to the cases, let's name them, respectively, as $B_1$, $B_2$ and $B_3$. If we also name $A := \{W<79\}$, then we have

$$P(A) = P(A \cap B_1) + P(A \cap B_2) + P(A \cap B_3)$$

Why? Here's a fancy drawing:

This is actually an extension of $P(A) = P(A \cap B) + P(A \cap B^c)$ known as, as you pointed out, the law of total probability, except I use the version that doesn't have conditional probability.

Thus, $W$ can be written as follows:

$$W = 0 \times 1_{B_1} + 100e^{-0.04T} \times 1_{B_2} + 0 \times 1_{B_3}$$

Now let's compute $P(A \cap B_1)$ and $P(A \cap B_3)$ by examining $A \cap B_1$ and $A \cap B_3$. Firstly, for $A \cap B_1$

$$A \cap B_1 = \{\omega | \{W(\omega) < 0.79\} \cap \{ 0 \le T(\omega) < 1.5 \}\}$$

We want to compute the probability of all the sample points $\omega$ satisfying both cases, i.e. sample points in both sets $A := \{W < 79\}$ and $B_1 := \{ 0 \le T < 1.5 \}$. Now if $\omega \in B_1$, then $\omega \notin B_2, \notin B_3$ by the very definition of partitions. Thus, for such an $\omega \in B_1$, i.e. $0 \le T(\omega) < 1.5$, this is what becomes of $W$ for this particular $\omega$:

$$W(\omega) = 0 \times 1_{B_1}(\omega) + 100e^{-0.04T(\omega)} \times 1_{B_2}(\omega) + 0 \times 1_{B_3}(\omega)$$

$$ = 0 \times 1 + 100e^{-0.04T(\omega)} \times 0 + 0 \times 0$$

$$ = 0 + 0 + 0 = 0$$

For this $\omega$ that is said to also in be $A$, i.e. $W(\omega) < 79$, we now have that $W(\omega) = 0 < 79$. This statement is always true. Hence for $\omega \in B_1$, $\{W < 79\} = \{0 < 79\} = \Omega$, i.e.

$$A \cap B_1 = \Omega \cap B_1 = B_1$$

It is not that $A = \Omega$ but rather when $A$ is intersected with $B_1$, $A$ might as well have been $\Omega$. This is because as it turns out $B_1 \subseteq A$, i.e. $$\{0 \le T < 1.5\} \subseteq \{W < 79\}$$

Thus, $$P(A \cap B_1) = P(B_1)$$ $$\to P(A) = P(A \cap B_1) + P(A \cap B_2) + P(A \cap B_3) = P(B_1) + P(A \cap B_2) + P(A \cap B_3)$$

Similarly, $$P(A \cap B_3) = P(B_3)$$

Thus, $$P(A) = P(B_1) + P(A \cap B_2) + P(A \cap B_3) = P(B_1) + P(A \cap B_2) + P(B_3)$$

Finally, let's examine $A \cap B_2$.

$$A \cap B_2 = \{\omega | \{W(\omega) < 79\} \cap \{ 1.5 \le T(\omega) < 8 \}\} = \{\omega | \{100e^{-0.04T(\omega)}1_{B_2} < 79\} \cap \{ 1.5 \le T(\omega) < 8 \}$$

$$= \{\omega | \{100e^{-0.04T(\omega)}1_{ 1.5 \le T(\omega) < 8 } < 79\} \cap \{ 1.5 \le T(\omega) < 8 \}\}$$

$$= \{\omega | \{100e^{-0.04T(\omega)} < 79\} \cap \{ 1.5 \le T(\omega) < 8 \}\}$$

$$= \{\omega | \{T(\omega) > \frac{\ln(0.79)}{-0.04}\} \cap \{ 1.5 \le T(\omega) < 8 \}\}$$

$$= \{\omega | \{8 > T(\omega) > \frac{\ln(0.79)}{-0.04} \}\}$$

Luckily, $A$ and $B_2$ were 'related' so they intersect nicely enough such that computing $P(A \cap B_2)$ is now simply a matter of computing the probability that $T$ falls in the interval $(\frac{\ln(0.79)}{-0.04},8)$

Therefore,

$$P(A) = P(0 \le T<1.5) + P(8 > T > \frac{\ln(0.79)}{-0.04}) + P(8 \le T<10)$$

Compare:

$$1 = P(\Omega) = P(0 \le T<1.5) + P(8 > T \ge 1.5) + P(8 \le T<10)$$

What do we learn from the comparison? It seems that the event $A$ is pretty big, i.e. $W<79$ with high probability. After all, it covers the entire range of $T$, which is $[0,10]$ except $(1.5,\frac{\ln(0.79)}{-0.04})]$. That makes sense since $W$ is $0$ for $\frac{(10-8) + (1.5-0)}{10-0} = 35$% of a uniformly distributed range.

Actually, we may compute

$$P(A) = 1 - P(1.5 \ge T < \frac{\ln(0.79)}{-0.04})) \approx 56.069 \ \text{%}$$

![https://i.sstatic.net/0g15I.png]](https://i.sstatic.net/0g15I.png]){kind=link}